European Union Sustainable Finance Regulatory Overview

September 13, 2022

Article by Benedict Jones Innovest Advisory.

In March 2018, the European Commission published the ‘Action Plan on Financing Sustainable Growth’. The Action Plan seeks to increase the role of financial services in the transition to a low carbon more sustainable economy through:

(1) reorienting capital flows towards sustainable investment;

(2) managing financial risks from environmental and social issues, and;

(3) fostering transparency and long-termism in financial activity.

Three key legislative initiatives as part of the Action Plan are of particular relevance to Fund Managers.

1. Sustainable Finance Disclosure Regulation (SFDR)

The SFDR introduces sustainability disclosure standards for financial market participants, advisers and products. The regulation requires all EU-based financial market participants (FMPs) or overseas FMPs marketing towards EU investors to disclose on sustainability related issues. Disclosure requirements are at both the entity level and product level.

The SFDR is framed as a series of sustainability-related disclosures which must be made:

- On the fund manager’s website;

- In the pre-contractual and periodic documentation for a financial product such as a fund or managed account.

Although not originally intended to be a product labelling scheme, the SFDR provides three classifications of financial products.

Article 6

Article 6 is the default classification of funds and refers to those with no specific process to integrate sustainability into investment decision making. These funds do not have a sustainable investment objective, nor do they explicitly target investments in assets which generate positive environmental or social outcomes

Article 8

To qualify as an Article 8 Fund, two requirements must be satisfied:

- Financial products must promote environmental and/or social characteristics, but do not explicitly have them as the overarching objective of the fund;

- Portfolio companies should follow good governance practices, with regards to sound management structures, employee relations, remuneration of staff and tax compliance.

Article 9

An Article 9 fund is “a fund that has sustainable investments as its objective”. To qualify as a sustainable investment, fund managers need to demonstrate that:

- Investments contribute to a sustainable investment objective;

- Investments do not significantly harm any other social or environmental objective (DNSH Principle);

- Investee companies follow good governance practices.

2. Regulatory Technical Standards

The Regulatory Technical Standards (RTS) provides clarifications and supplementary detail to the SFDR. Of particular relevance to fund managers with products seeking to become Article 8 or Article 9 are the final prescribed templates for:

- Pre-contractual disclosures

- Periodic Reports

- Principle Adverse Impact (PAI) Statements.

These additional disclosures will come into effect on 1st January 2023. To date, firms have been required to comply with SFDR on a best effort basis, but firms will likely gravitate towards using these templates sooner.

3. Taxonomy Regulation

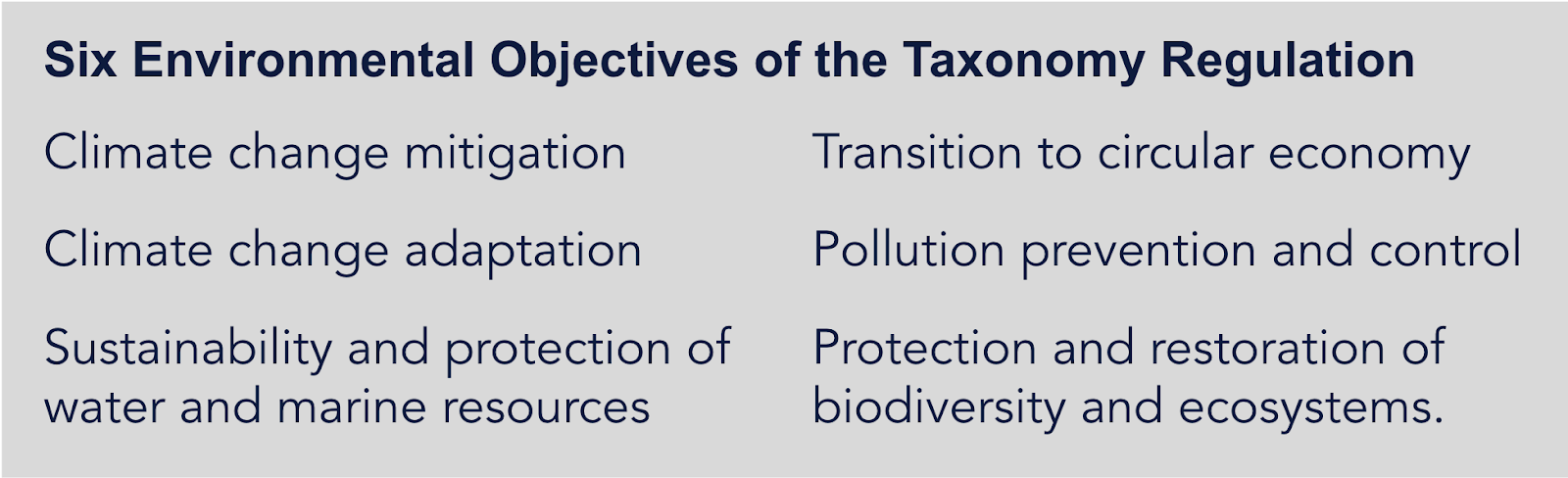

The Taxonomy Regulation, often called the ‘Framework Regulation’ provides a common language or classification system used to determine the degree to which an economic activity can be considered as ‘environmentally sustainable’. An economic activity will be considered “environmentally sustainable” if it:

- Contributes substantially to at least one of six environmental objectives;

- Does no significant harm to any of the other environmental objectives (DNSH Principle)

- Complies with minimum social safeguards

- Complies with certain specific performance thresholds denoted in the “Technical Screening Criteria”.

Innovest Sustainable Finance Advisory Services

EU Taxonomy Eligibility and Alignment

For fund managers wishing to align to the EU Taxonomy, Innovest analyses pipeline and portfolio companies to determine their eligibility and alignment to the EU Taxonomy. We assess which of the six environmental objectives of the Taxonomy a company aligns to, and importantly which activity under this it meets. We also assess whether companies meet the Do No Significant Harm criteria and the Minimum Safeguards to provide a robust opinion on Taxonomy alignment.

SFDR Readiness Assessment

To prepare for SFDR Article 9 Disclosure, or to respond to increasing investor enquiries, Innovest provides a SFDR Readiness Assessment of fund managers. We review a fund’s pre-contractual disclosures, sustainability policy, website disclosures, marketing materials, sustainability data collection and other supporting documents and undertake a gap analysis of the extent to which the fund meets the SFDR Article 9 requirements. We provide recommendations on steps needed to become fully compliant. We are able to support the fund manager to implement these steps if desired.

PAI Data Integration

Principle Adverse Impacts (PAIs) are negative, material, or likely to be material effects on sustainability factors that are caused, compounded by, or directly linked to investment decisions. Article 9 compliant fund managers will need to collect extensive PAI data from their underlying portfolio companies. Innovest supports fund managers to integrate this data collection into their existing processes and systems, streamlining the PAI’s with their existing KPI and metric collection. We develop bespoke data collection tools suitable for portfolios of any size, and can support the collection, analysis and reporting of this data.

Preparation of SFDR Disclosure Statements

Innovest supports fund managers in the drafting of SFDR Disclosure Statements. In such an early stage of the implementation of SFDR Regulations and Disclosures, we bring our expert knowledge of the evolving best practice in this field to accurately and robustly present a fund managers alignment to SFDR in a Disclosure Statement. We also offer a review service, providing critical review and recommendations on draft disclosure statements.